What needs to happen to create a future in which we all agree that wellbeing is critical and identify the obstacles on the way?

8. Who do you think should take responsibility for educating and engaging employees on financial matters such as mortgages, savings, insurance, and retirement planning? 9. How important do you feel your duty is to provide education and guidance to your employees to support their financial wellbeing 10. Do you currently offer any financial education/support/wellbeing to your employees? 11. Does your business provide any pre-retirement or financial guidance to employees approaching the age when they can access their pension pots (age 55+)? 12. Are you aware of what you can do to support your employees’ financial wellbeing? 13. What financial guidance, support or advice do you believe would be most beneficial for your employees to receive? 14. Do you believe that your business would have any concerns about providing employees with access to financial support, education and advice provided by an external financial adviser 15. Why do you have concerns?

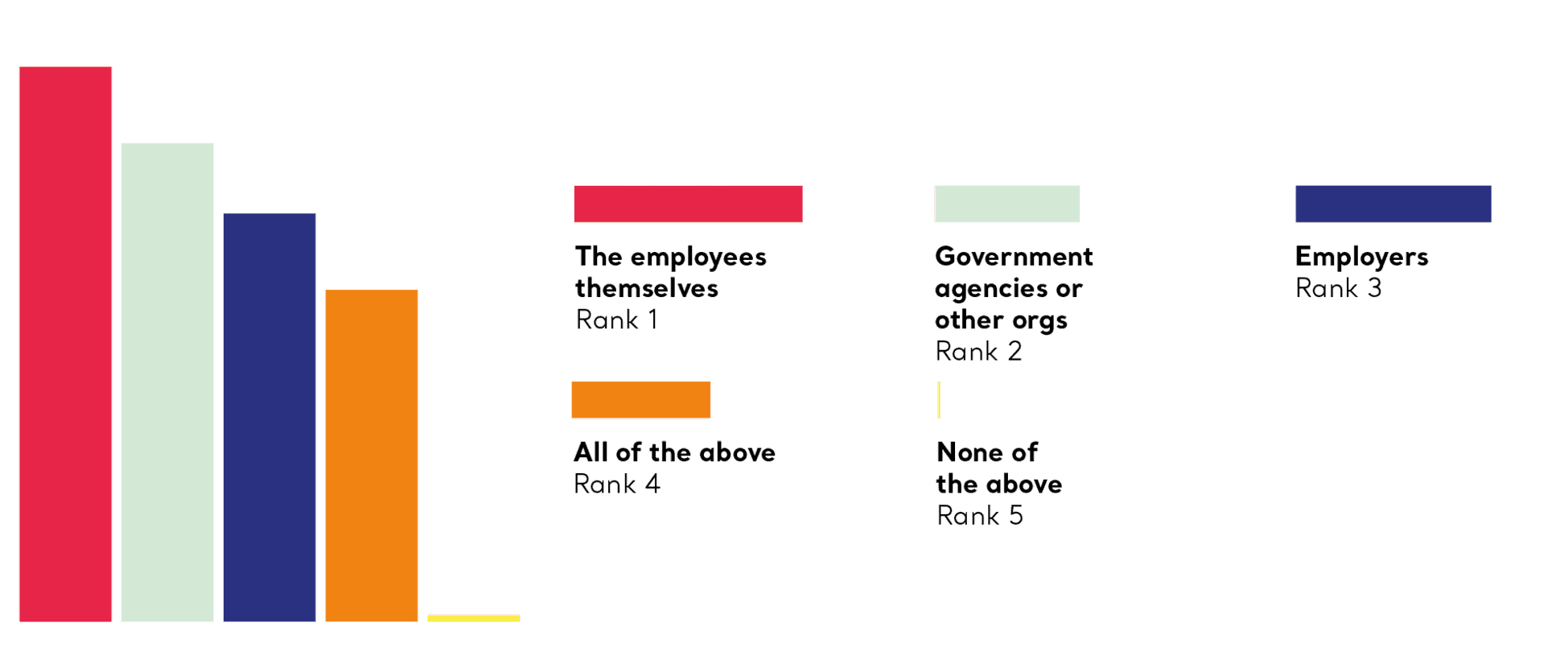

These results point to a disconnect. While employers agree it will help their people and, ultimately, their organisation, most see it as the personal responsibility of their staff first and foremost. After that, it is seen as something companies and government should shoulder.

Starkly, only one per cent of respondents felt it was important for them, as an employer, to fill in the evident gap for their staff to access financial well being. Collectively, 83 per cent did not see it as a business priority. While this is at odds with our headline finding that companies value financial well being as a benefit for their people, it does explain why organisations struggle to define and deliver what it is.

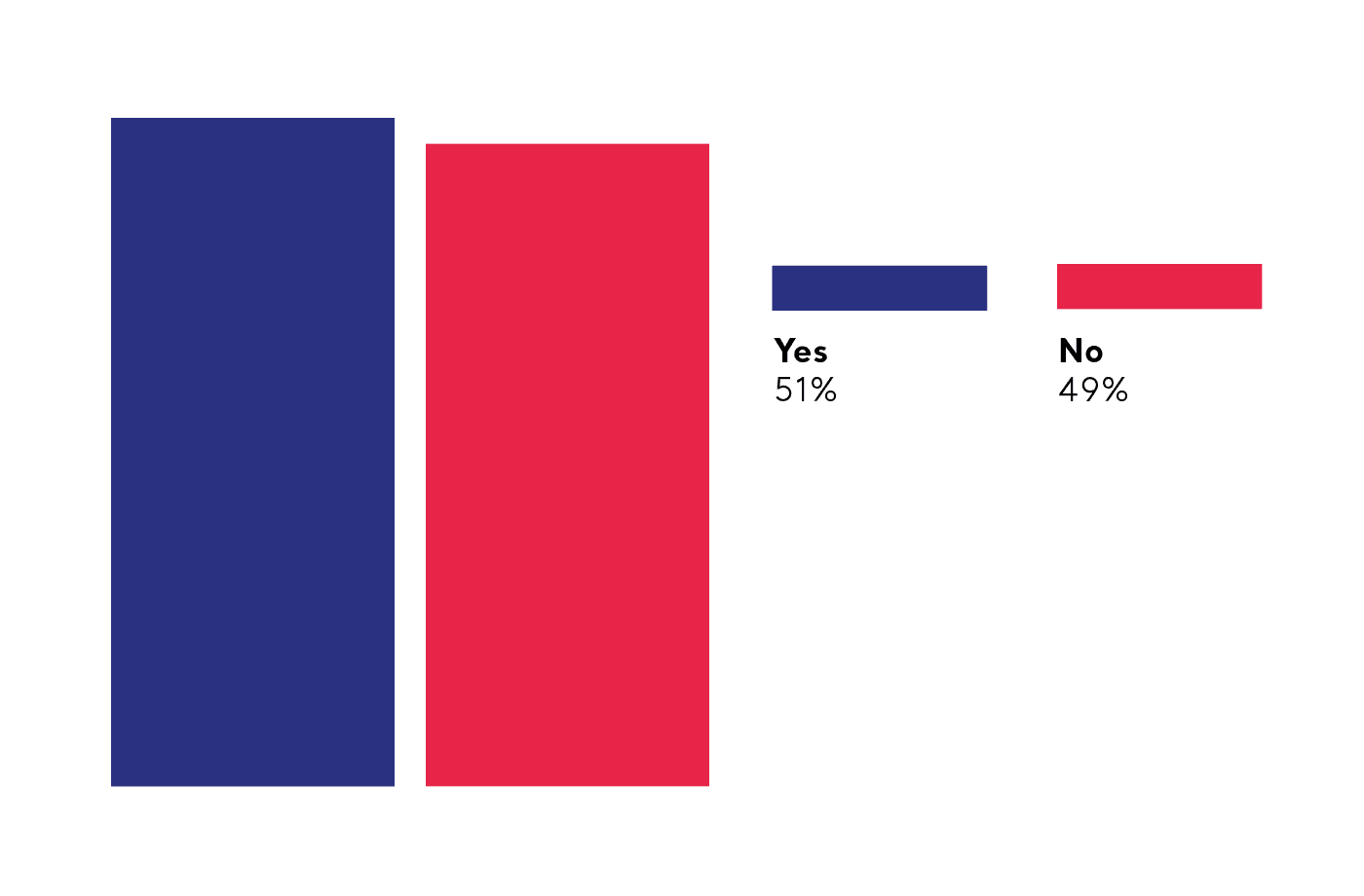

Starkly, 50.5 per cent do but 49.5 per cent do not. There’s a fair amount of detail in the responses, ranging from tailored sessions, employee assistance programmes and pre-retirement sessions. But that’s only from half the companies questioned.

Of those businesses that do offer guidance to employees, for the majority this takes the form primarily of employee assistance programmes. However support also comes in the form of workshops, free access to financial advice, sessions on pensions and more. The word cloud below illustrates some of the buzzwords used by respondents to this question.

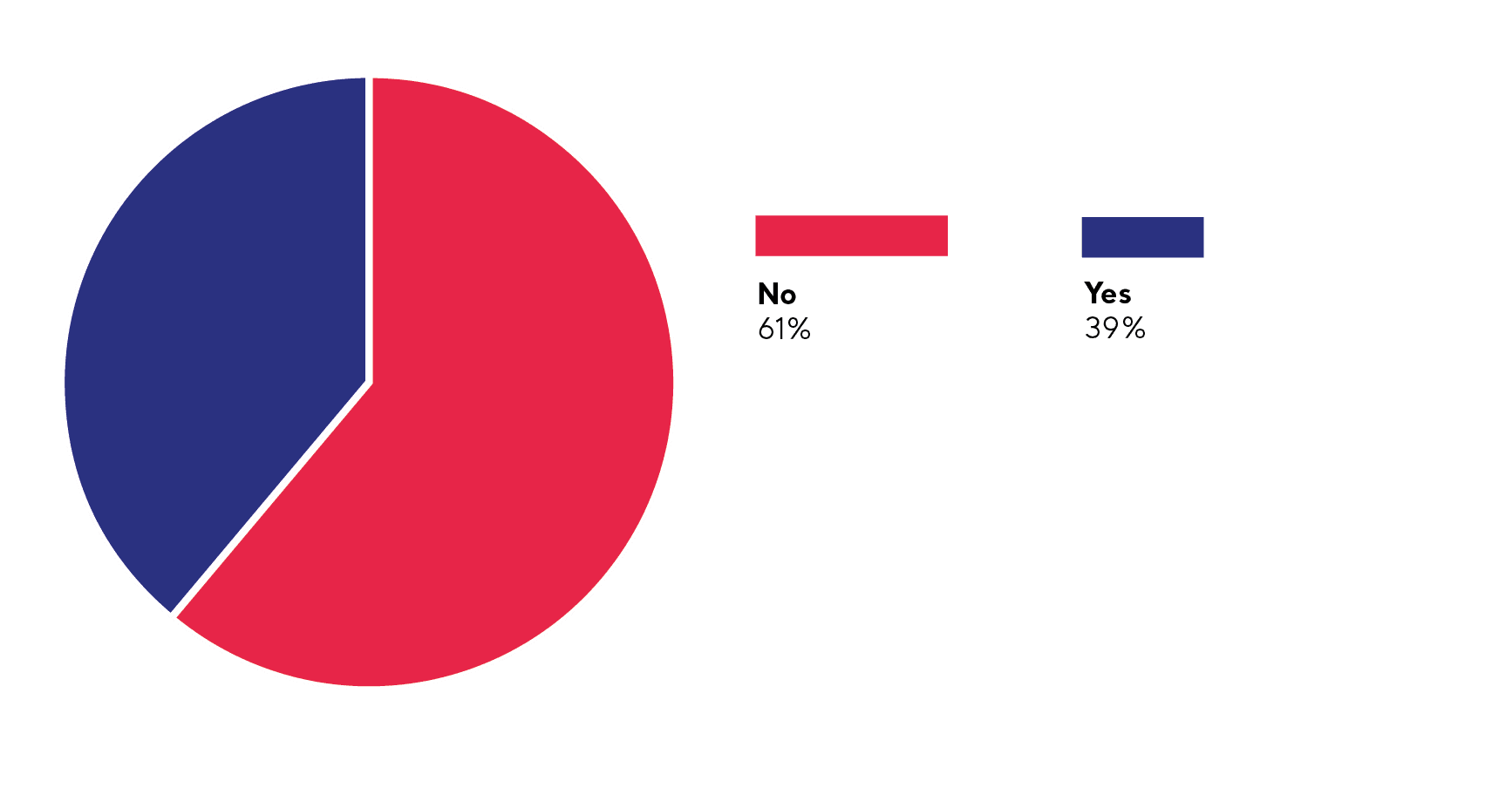

The majority (61 per cent) don’t but 40 per cent do, largely in partnership with advisors, brokers or pension scheme managers. Why are these methods not deployed by other companies?

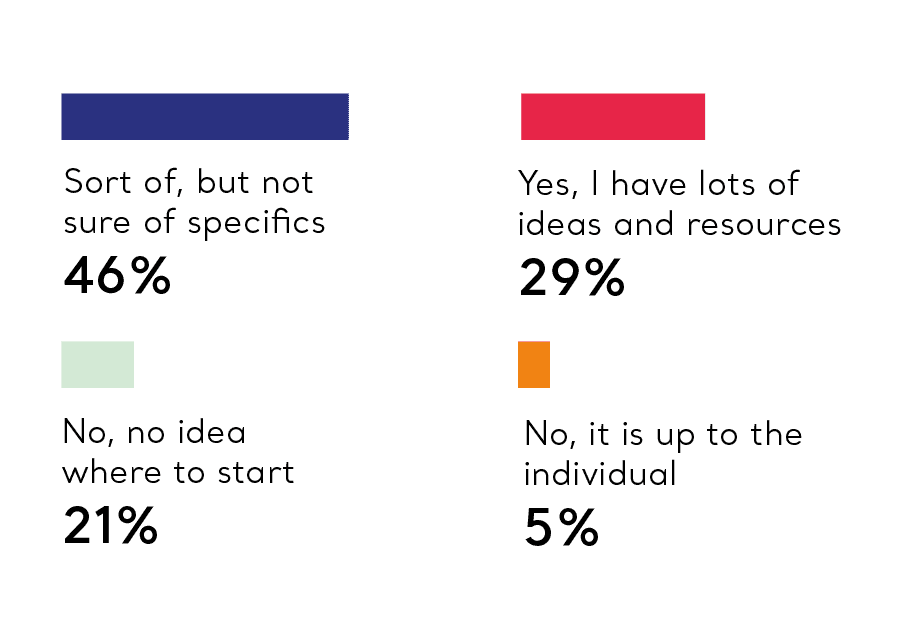

Just under one in three (29 per cent) said they had a firm idea and the resources to help their staff but the majority either didn’t feel it was their responsibility (five per cent) or had little idea of where to start.

Again, this speaks to the dominant theme that while employers backed better access and greater understanding of financial matters for their employees, they remained unsure of what to do to make it happen.

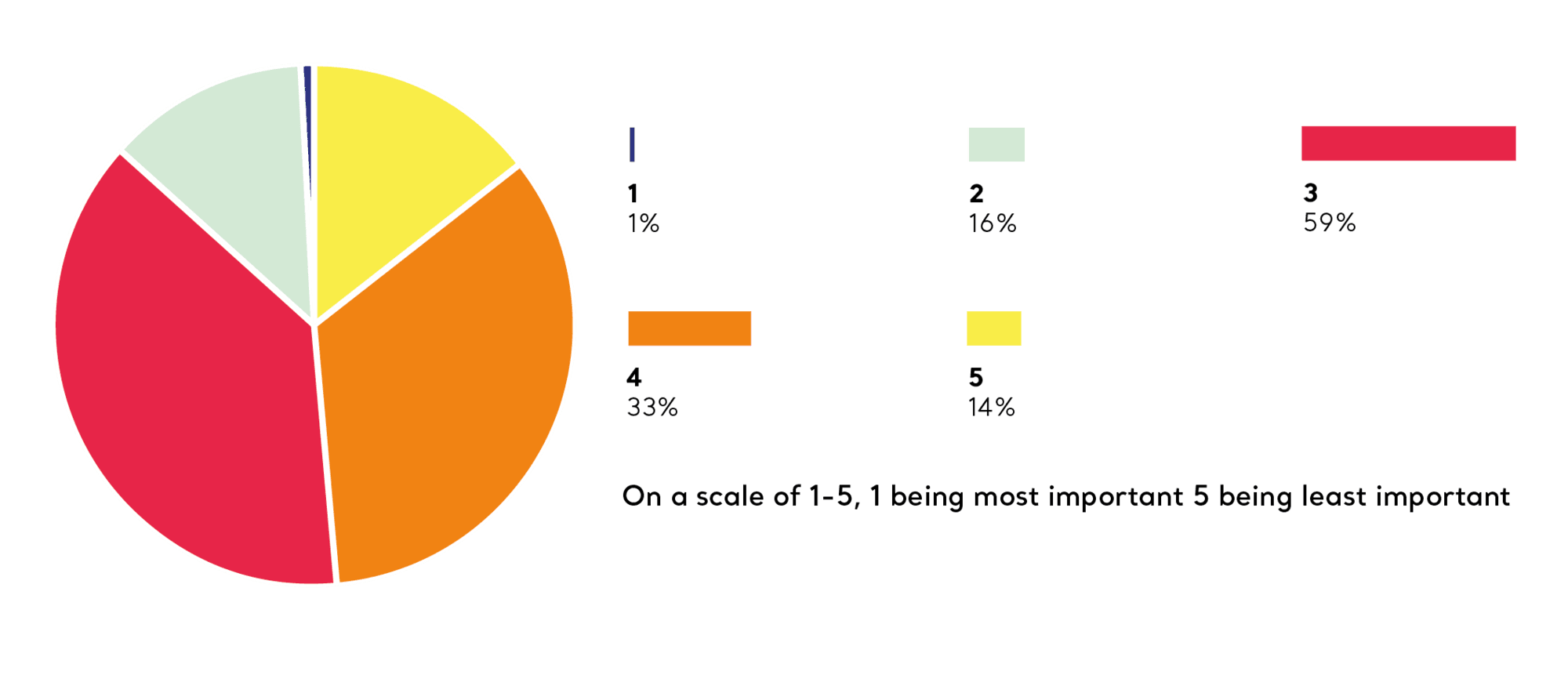

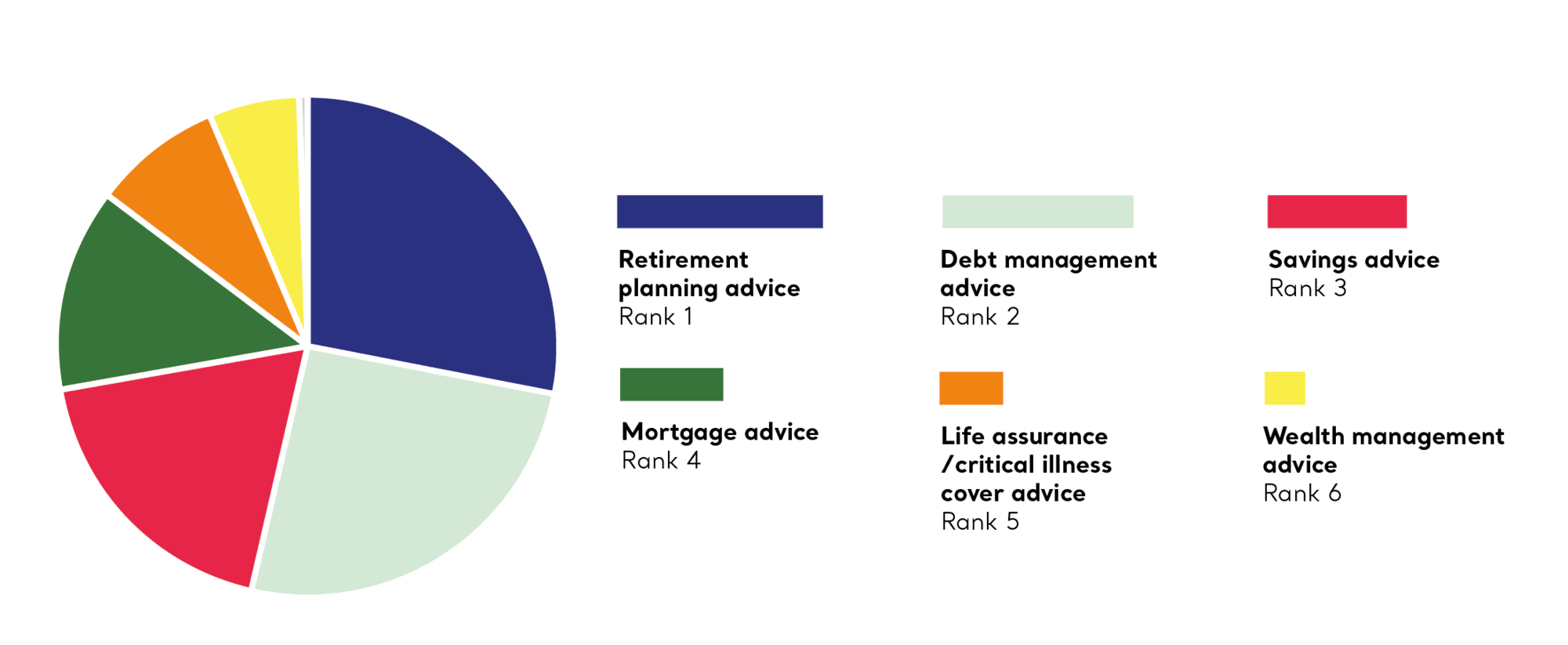

Retirement planning, followed by debt management and savings advice were the top three. If all three were addressed with the right advice and infrastructure, how far would they go to making financial wellbeing a more concrete reality?

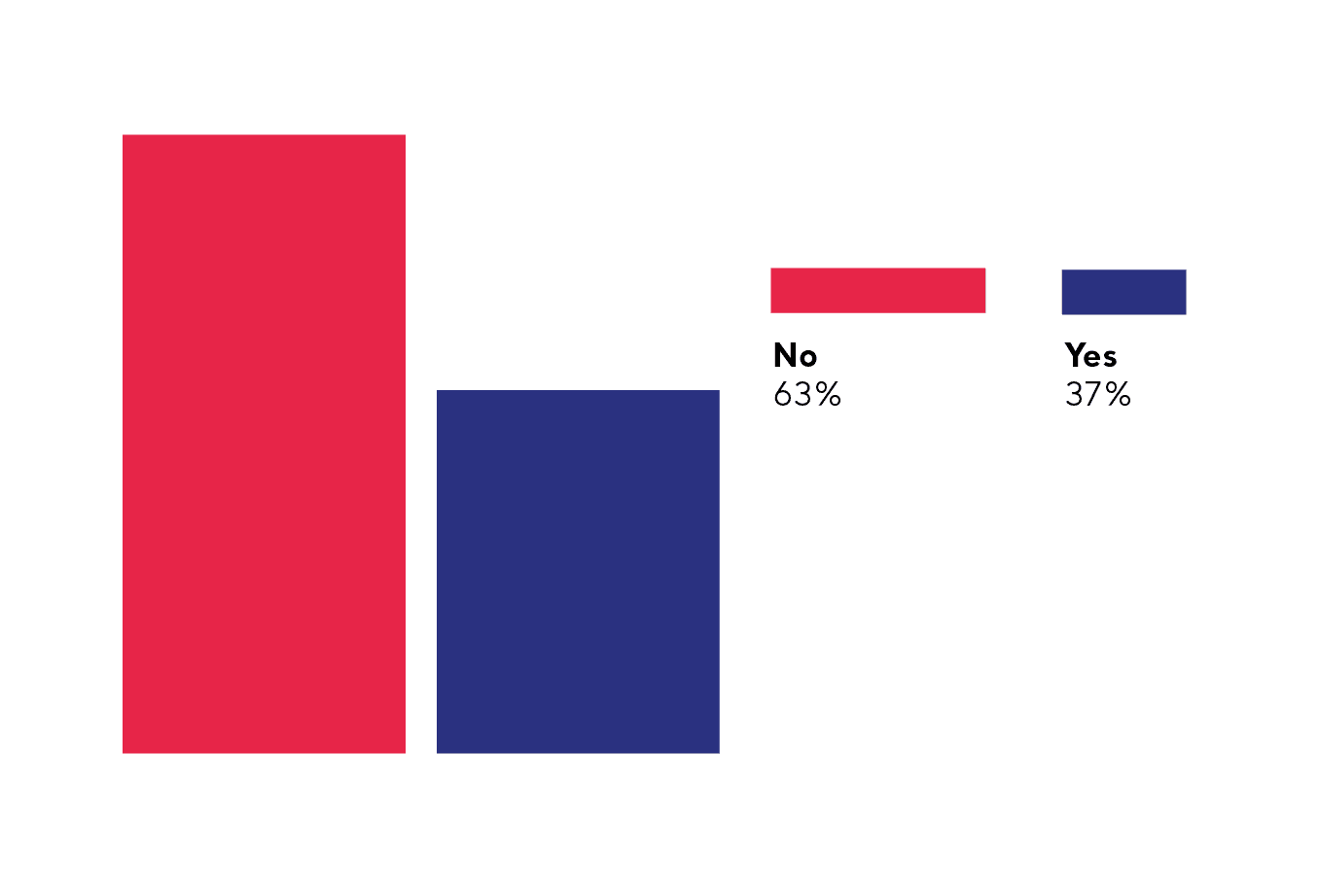

Better news for employees in that 63 per cent would not have any concerns in working with an external company to meet what appears to be evident demand for the above. If they’ve not already done so, what prevents them from putting the wheels in motion?

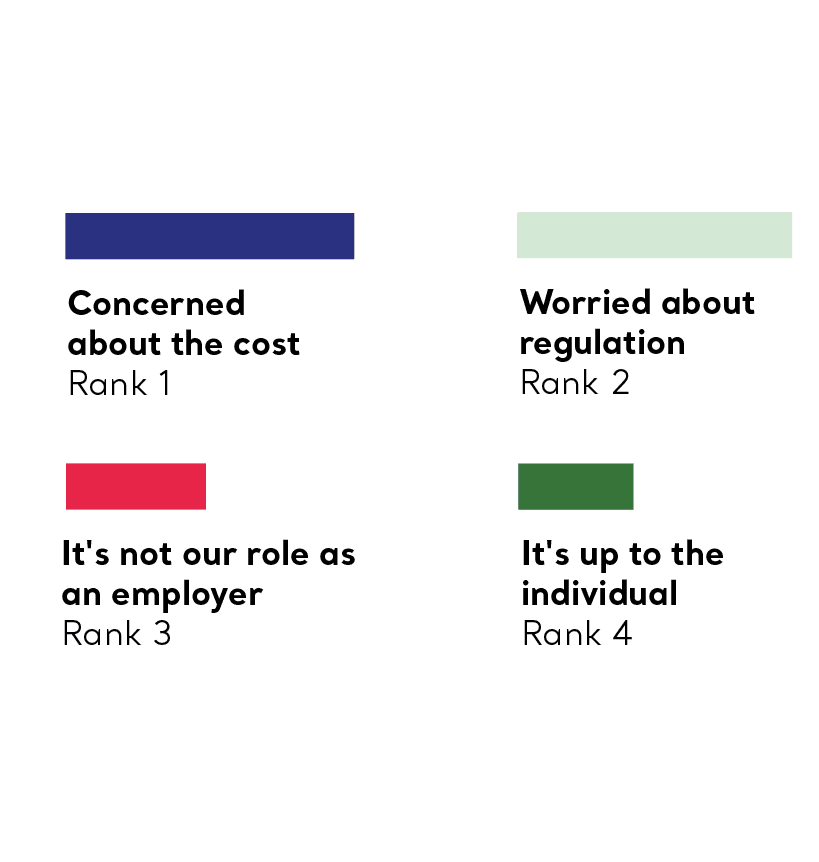

Of those who did, the main reasons were worries about the cost (61 per cent) and fear of falling foul of regulation (58 per cent).

Our only rejoinder to this would be: if you take care to work with the right advisor, they can ensure that these hazards are dealt with sensibly.