As I’ve already said, some different ideas are to be expected.

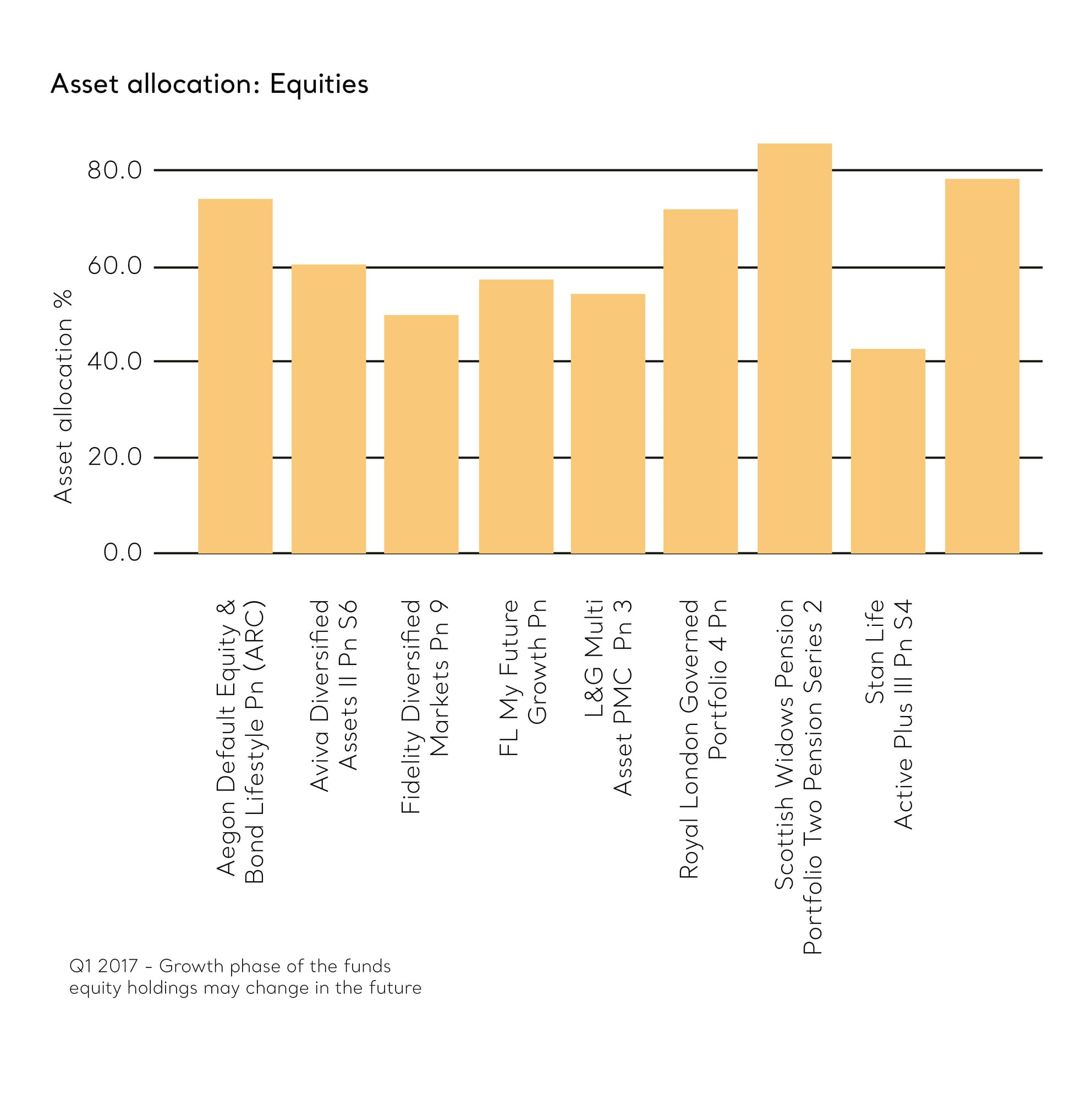

So why does this variety cause a problem? The answer lies in how volatile each of these funds are – in other words, how big the swings on investment gains and losses are designed to be.

So why does this variety cause a problem? The answer lies in how volatile each of these funds are – in other words, how big the swings on investment gains and losses are designed to be.

That’s related in part to how much risk each fund is willing to take, which in turn depends on the investment return they’re trying to achieve. Again, you’d expect every default fund to have a similar level of volatility. That’s just not the case. Some funds are conservative, others are far more aggressive.

They don’t measure themselves in similar ways either – it’s a case of apples and oranges unfortunately. The chances are, you were sold your pension scheme complete with the default fund ready to invest in. Perhaps you got lucky, and your provider’s fund is one of the better ones we’ve analysed.

Others, frankly, should be cursing their luck. Even if you are in a “good” fund though, it might not be suitable for your workforce.